A Terrible, Terrible Week in Software Stocks. But Not Necessarily a Terrible 12 Months. | SaaStr

This week was bad. Really bad. And Thursday was particularly brutal. ServiceNow was down 15-17% at the open. IBM off 10%. Salesforce down 7%. Oracle down 5%....

TechnologyInnovationBest PracticesGuideTutorial

Listen to Article

0:00

0:00

0:00

A Terrible, Terrible Week in Software Stocks. But Not Necessarily a Terrible 12 Months. | Saa Str

Overview

AI VC

AI Mentor: Digital Jason + Amelia

AI Startup Benchmarking

AI Agent Playbook

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

Details

University

All Posts

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2026 (Free)

Speaker Submissions

Speaker Requirements

Overview

A Terrible, Terrible Week in Software Stocks. But Not Necessarily a Terrible 12 Months.

This week was bad. Really bad. And Thursday was particularly brutal.

Service Now was down 15-17% at the open. IBM off 10%. Salesforce down 7%. Oracle down 5%. Intuit down 7%. And the carnage spread to almost every major B2B name.

The trigger was earnings from two of the biggest legacy software names. Both beat. Both guided cautiously. And in April 2026, that’s all it takes to get obliterated.

Service Now reported Q1 revenue of

3.77B,aheadofthe

3.74B consensus. They still dropped 15%.

A 75 basis point subscription revenue headwind from on-premises deal slippage in the Middle East (~$23M), tied to the Iran conflict

Full-year adjusted operating margin guidance cut from 32% to 31.5%

No mention of their “generative AI book of business” metric, which sat at $12.5B at the end of 2025

IBM had its own problem. Revenue growth slowed to 9% from 12.2% the prior quarter. Software segment growth decelerated to 11.3% from 14%. That was enough for a 10% haircut, layered on top of the 13% single-day drop in February when Anthropic demonstrated Claude Code could modernize COBOL.

The read-through hit everything. Truist cut Service Now’s price target from

125to

120 and wrote that “with heightened scrutiny on software vendors as frontier labs ramp enterprise revenue, the penalty for missteps becomes more severe.”

That’s the new reality. Beat and guide cautiously? Down 15%. Miss on anything? Down more.

5 Interesting Learnings from Service Now at $14.7B in ARR: 22% Growth, Rule of 54, and the Paradox of Beat-and-Lose

5 Interesting Learnings from Service Now at $14.7B in ARR: 22% Growth, Rule of 54, and the Paradox of Beat-and-Lose

Pull up the year-to-date board and it’s a sea of red. Out of 25 major B2B names:

Only Digital Ocean (+96%) is meaningfully green YTD. Almost every other name that touches B2B workflows is off 20% to 75% in under four months.

That’s what a sector-wide re-rating looks like. The i Shares Expanded Tech-Software ETF (IGV) went from an all-time high of

117to

85. Software collectively entered bear market territory in early February and hasn’t climbed out.

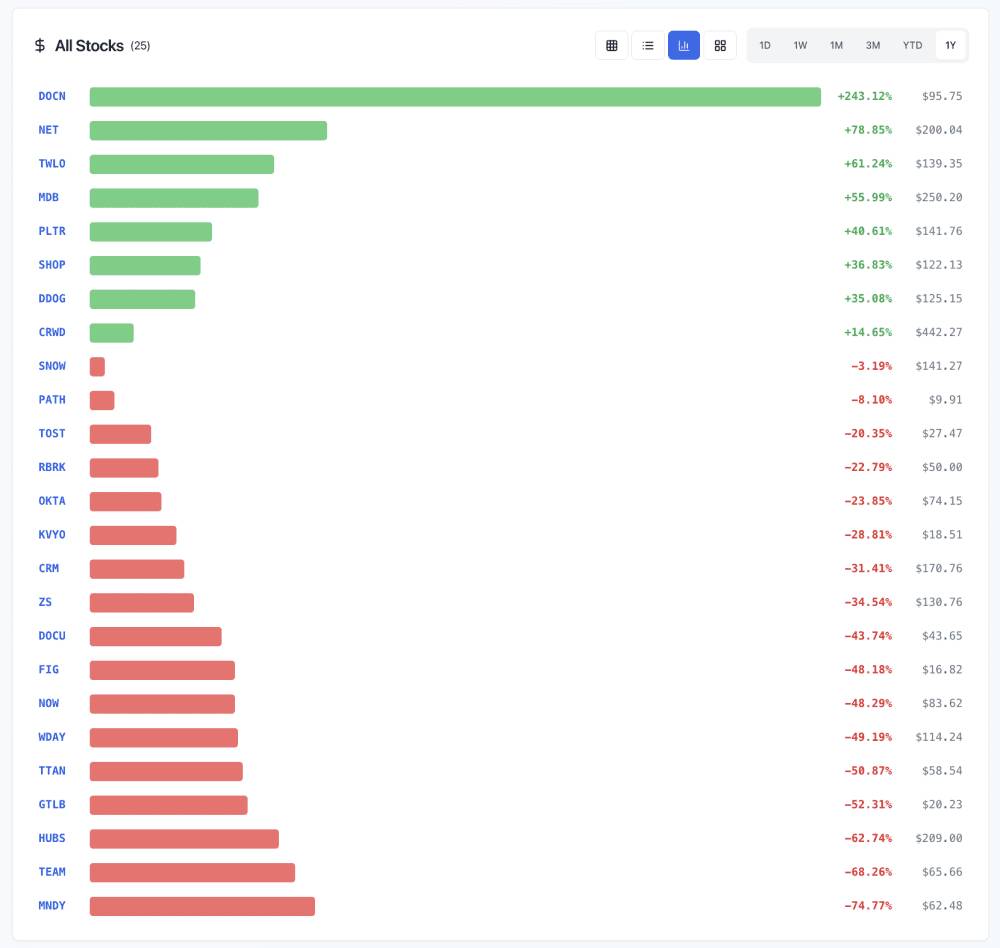

But Zoom Out to 12 Months and Something Different Shows Up

Switch the chart to 1-year and the picture changes materially. A lot of these same names are still up, in some cases massively:

Even Snowflake, after all the carnage, is only -1.89% on a trailing 12-month basis. Palantir has been the single rare name that’s held up all year as its “Foundational Operating System” positioning gets re-rated as an AI enablement story rather than a disruption target.

The stocks that are down 12 months are mostly the ones the market has decided are most exposed to AI displacement risk: workflow tools, collaboration, document signing, anything where the core value prop is seat-based Saa S and the use case can be plausibly absorbed by an agent.

The stocks that are up are infrastructure, security, data, and AI-native platforms. Companies selling picks and shovels to AI, or companies whose product gets more valuable as agents proliferate.

The market isn’t saying software is dead. It’s saying two very specific things:

Infrastructure beneath AI is the protected category. Cloudflare, Mongo DB, Datadog, Digital Ocean, Crowd Strike are all up meaningfully because every new AI workload needs edge compute, databases, observability, and security. More agents means more infrastructure consumption, not less.

Service Now’s own response is instructive. They’ve introduced an “Agentic ACV” tier where customers pay for tasks completed by AI agents rather than per-seat. That’s the pivot every B2B company is being forced into right now, whether they want it or not.

A 12-month recovery in names like DOCN (+234%), NET (+79%), TWLO (+62%), MDB (+56%), and PLTR (+44%) means the narrative “AI is killing software” is too simple.

AI is killing one specific business model: charging $50-150 per seat per month for software that increasingly looks like something a model can do.

AI is minting a different business model: usage-based consumption of infrastructure, security, and data platforms that AI itself requires at 10x the prior scale.

The sorting is happening in real time. This week’s Service Now earnings reaction is part of that sorting. So was IBM’s COBOL moment in February. So was the broad Anthropic Cowork sell-off. The companies that figure out how to reprice, reposition, and turn agents from a threat into a wedge are going to look very different 18 months from now than they do in today’s red screen.

A Sector That Feels Dying, But Really is Just Being Rebuilt

If you’re holding B2B stocks right now, the YTD number is painful but not the most informative metric. The ones to watch are:

Are they shifting from seat-based to outcome or consumption pricing?

Is their “AI book of business” growing, shrinking, or quietly disappearing from the earnings deck?

Are they acquiring into AI-native categories or defending a shrinking moat?

Today was brutal. The 12-month chart tells you which names have already answered those questions and which ones are about to find out the hard way.

Either way, this isn’t a sector dying. It’s a sector being rebuilt with very different rules, at very different multiples, with a very different set of winners.

The New AI Paradigm: Great Outbound, Terrible Follow Up

Negotiating Comp on the Way In Is Smart. Even Better is Doing It 12 Months In.

The New AI Paradigm: Great Outbound, Terrible Follow Up

Negotiating Comp on the Way In Is Smart. Even Better is Doing It 12 Months In.

RSS Industry News

Get from

0to

100 Million in ARR

with less stress and more success.

Key Takeaways

AI VC

AI Mentor: Digital Jason + Amelia

AI Startup Benchmarking

AI Agent Playbook

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Cut Costs with Runable

Cost savings are based on average monthly price per user for each app.

Which apps do you use?

Apps to replace

ChatGPT

$20 / month

Lovable

$25 / month

Gamma AI

$25 / month

HiggsField

$49 / month

Leonardo AI

$12 / month

TOTAL$131 / month

Runable price = $9 / month

Saves $122 / month

Runable can save upto $1464 per year compared to the non-enterprise price of your apps.